Federal Student Aid Changes Effective

July 1, 2026

The Working Families Tax Cuts Act (formerly known as the One Big Beautiful Bill - OB3) was signed into law on July 4, 2025. It brings significant changes to how students and families pay for college, starting July 1, 2026. Those changes, as we know them currently, are summarized below by type of aid.

As the Department of Education (ED) releases further guidance and finalizes the rules, we will continue to update this page with the most accurate and actionable information available. We understand that students, families, and others have questions, and we are here to help.

Legacy Students

There are legacy provisions put in place to allow current students to continue borrowing under previous rules while in a continued degree program. Below are the three criteria a student must meet to be considered a legacy student.

- Student must have been enrolled in their program of study before July 1st, 2026. Student cannot have withdrawn or ceased enrollment in their program before July 1st, 2026.

- Student must have received any direct loan disbursement (unsub or GRAD PLUS) for their program of study before July 1st, 2026.

- Student must be within their expected time to credential (please see Time to Credential tab).

Federal PLUS Loan Changes

Parent PLUS Loans will continue to to be available, but new borrowing limits will apply. Some students will be able to qualify for legacy protections. See the legacy section above for more details.

New Annual Limit

- Parents may borrow up to $20,000 per student, per year.

New Lifetime Limit

- Parents may borrow up to a total of $65,000 per student in total

Under the New Rules

- Families who borrow $20,000 per year could reach the $65,000 lifetime limit before a student completes four years of undergraduate study.

New Proration Rules

- PLUS Loan eligibility is tied to the student's cost of attendance and enrollment level. If a student is enrolled less than full-time, the PLUS loan amount borrowed will be prorated (reduced).

Graduate PLUS loans will be eliminated for enrollment periods that begin on or after July 1, 2026. This means:

- New Graduate/Professional students will no longer be able to borrow Graduate PLUS loans for any new academic term that starts on or after July 1, 2026.

- Graduate students will instead need to rely on Federal Direct Unsubsidized Loans and any other available funding options, such as private loans

- Some graduate students may qualify for legacy protection. See legacy section above for more details.

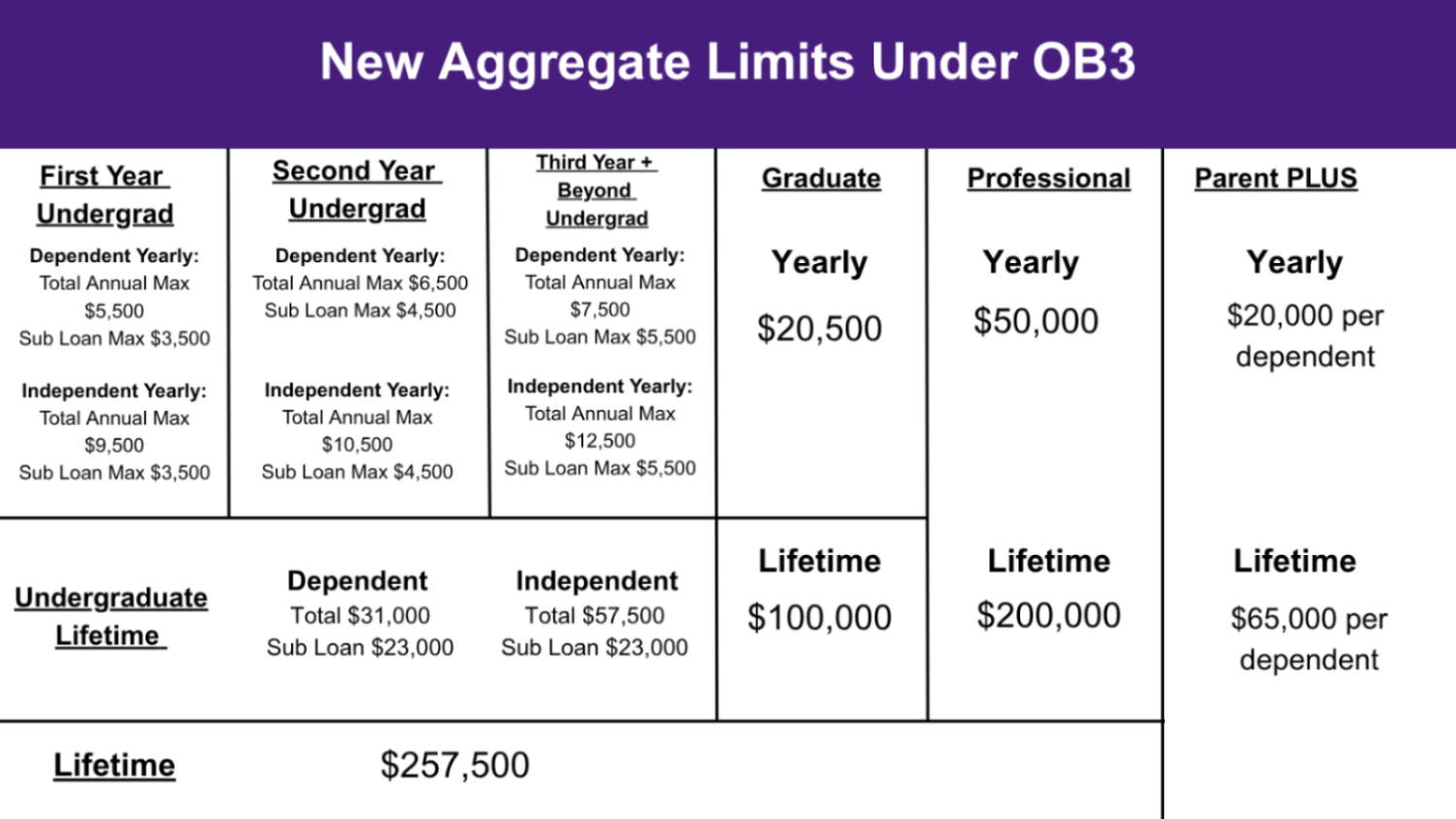

Loan Limit Changes

The One Big Beautiful Bill Act (OB3) introduces new federal loan limit provisions that may affect how much students and parents can borrow through federal student loan programs. These changes include updates to annual and lifetime borrowing caps and may vary by loan type and academic program.

Students and families should review the revised limits carefully to understand how future borrowing eligibility may be impacted. Detailed information about the updated loan limits is provided below.

For students enrolled in graduate degree programs (such as a master’s or doctoral program that is not classified as a professional program):

-

The annual Federal Direct Unsubsidized Loan limit will remain $20,500 per year, which is the same as the current annual limit.

-

A new lifetime loan limit of $100,000 will apply.

The lifetime limit means the maximum total amount you can borrow for graduate study over time.

Important:

-

This $100,000 limit applies only to graduate-level borrowing.

-

This new limit does not include any loans you borrowed as an undergraduate student.

What degree is considered professional has been re-defined by the Department of Education, not LSUHSC.

LSUHSC's professional degrees are:

- Medicine

- Doctorate of Dental

For students enrolled in professional degree programs:

-

The annual Federal Direct Unsubsidized Loan limit will be $50,000 per year.

-

The lifetime loan limit will be $200,000.

This $200,000 limit includes all graduate and professional borrowing combined, but:

-

This new lifetime limit does not include loans borrowed during undergraduate study.

In addition to the limits listed above, there will be a new lifetime borrowing cap of $257,500.

This lifetime cap:

-

Includes all federal student loans borrowed for undergraduate, graduate, and professional study combined.

-

Does not include PLUS loans.

-

Includes loan amounts even if they have already been repaid, forgiven, or discharged.

This means the total amount you borrow over your lifetime will count toward this cap, even if you no longer owe the full amount.

Less-Than-Full-Time Loan Adjustments

The One Big Beautiful Bill Act (OB3) includes provisions that affect federal student loan eligibility and borrowing amounts for students enrolled less than full-time. This adjustment is referred to as the Schedule of Reduction. Students who plan to enroll part-time should review the information below to understand how these changes may affect their federal loan options.

Beginning with the 2026–2027 award year, if a student is enrolled less than full-time in an eligible program, their annual Federal Direct Loan limit will be reduced based on the number of credits they are taking compared to full-time enrollment.

The reduction:

- Is proportional to the student’s enrollment level

- Is based on the student’s enrollment status when the school determines loan eligibility at disbursement

- Is rounded to the nearest whole percent

In short:

If you are not enrolled full-time, you cannot borrow the full loan amount. Your annual

loan amount is reduced based on how close you are to full-time enrollment.

These proportional loan adjustments apply to:

-

All undergraduate, graduate, and professional student Direct Loan borrowers—Direct Subsidized Loans , Direct Unsubsidized Loans, and graduate PLUS Loans (for legacy borrowers).

- Parent PLUS Loans are not subject to these adjustments.

Full time enrollment for undergraduate students at LSUHSC is 12 hours per each semester.

An undergrad student is enrolled in:

- 7 credit hours in the fall

- 12 credit hours in the spring

- This equals 19 credit hours for the full academic year

Calculating the Reduction

- 19 (total year credit hours)/24 (full time) = 79%

- This means the student is enrolled at 79% of full-time status for the academic year

Apply that percentage to the annual loan limit

- For this example, this studsent is eligible for $7,500 if enrolled in full time for both semesters

- $7,500 x 79% = $5925 = new maximum loan amount the student is eligible for.

- The student's annual loan eligibility may be reduced equally or proportionally based on what is best for the student.

Repayment Plans for Student Borrowers

For Federal Student Loans Made on or After July 1, 2026

- Some existing repayment plans will end July 1, 2028 (ICR, PAYE, and SAVE).

- A new income based repayment plan (Repayment Assistance Plan, or RAP) will be created. Payments under this plan will

be determined based upon several factors:

- payments may be as low as $10/month,

- adjusted for dependents,

- and possibly forgiven after 30 years of payments.

- A new standard repayment plan will be created. Payments under this plan will have 4 fixed terms of 10, 15, 20, or 25 years (based on the amount borrowed).

- Current Borrowers:

- If no new loans are made on or after July 1, 2026, you are eligible to enroll in the current Standard, Graduated, Extended, or income based (IBR) repayment plan, or you may opt into the new RAP.

- If you are currently enrolled in ICR, PAYE, or SAVE, you must transition to a different repayment plan by July 1, 2028, (either current income based repayment plan, current standard plan, or RAP). If no selection is made, you will be moved to RAP automatically.

- It's important to note that all loans must be repaid under the same plan. So, borrowers with loans made before July 1, 2026, who take out additional loans on or after July 1, 2026, will only have RAP and the new standard plan to choose from.

- New Borrowers: For loans made on or after July 1, 2026, there will be two repayment plan options - the new standard repayment plan or RAP. If no selection is made, you will be assigned to the new standards payment plan.

Repayment Plans for Parent Borrowers

For Federal Parent PLUS Loans Made on or After July 1, 2026

A new standard repayment plan will be created. Payments under this plan will have 4 fixed terms of 10, 15, 20, or 25 years (based on the amount borrowed).

- Current Borrowers:

- If no new loans are made on or after July 1, 2026, you are eligible to enroll in the current Standard, Graduated, Extended, or income based (IBR) repayment plan.

- If you borrowed prior to July 1, 2026, AND subsequently borrow after July 1, 2026, repayment for all loans must be under the same payment plan which is the new standard payment plan.

- New Borrowers: For loans made on or after July 1, 2026, they can be repaid using only the new standard plan to choose from.

Deferment & Forbearance

The One Big Beautiful Bill Act (OB3)includes updates to federal student loan deferment and forbearance provisions. These changes may affect eligibility criteria, qualifying circumstances, and the length or availability of certain temporary relief options. Borrowers should review the information below to understand how these updates may impact their ability to pause or temporarily reduce loan payments. Specific repayment questions should be directed to your federal loan servicer.

-

Economic hardship deferment will no longer be available.

Borrowers with loans made on or after July 1, 2027, will not be able to pause their payments due to financial hardship under the economic hardship deferment option. -

Unemployment deferment will no longer be available.

Borrowers with loans made on or after July 1, 2027, will not be able to pause their payments due to unemployment under the unemployment deferment option. -

Forbearance will be limited.

For loans made on or after July 1, 2027, you may only receive forbearance for a maximum of nine months within any two-year period.

Forbearance allows you to temporarily pause or reduce your payments, but interest may continue to accrue during this time.

These changes apply only to federal student loans made on or after July 1, 2027.

If your loan was made before July 1, 2027, you will still have access to the current deferment options available under existing regulations.

Loan Rehabilitation

The One Big Beautiful Bill Act (OB3)includes updates to federal student loan rehabilitation provisions for borrowers in default. These changes may affect eligibility requirements, the rehabilitation process, and how defaulted loans are restored to good standing. Borrowers considering rehabilitation should review the information below to understand how these updates may impact their options for resolving default and regaining federal student aid eligibility. Specific repayment questions should be directed to your federal loan servicer.

- You can rehabilitate a defaulted federal student loan two times instead of just once

- Currently, borrowers are only allowed to rehabilitate a loan one time. Starting July 1, 2027, you will be allowed to complete the rehabilitation process twice if your loan goes into default more than once.

- The minimum monthly payment required during rehabilitation will increase from $5 to $10 dollars.

- If your calculated rehabilitation payment amount is very low, the minimum you will be required to pay each month will increase to $10.

- You must make nine on-time monthly payments within ten consecutive months. Missing a payment or paying late could restart the process.

- If you previously returned your loan to good standing through the Fresh Start initiative, that action does not count as using one of your rehabilitation opportunities.

Other Loan Changes

The OBBBA also included some changes about consolidation loans, deferment options, and forbearance that we will provide in the future as ED clarifies details. At this time, those will not be effective until July 1, 2027.

Additional Provisions of OBBBA

FAFSA Asset Exemptions: Starting with the FAFSA for aid year 2026-2027, the exemptions for assets of a family farm and a family-owned small business in the SAI calculation will be reinstated. Additionally, those asset exemptions will be expanded to include family-owned commercial fisheries.

Foreign Income for Pell Eligibility: Starting with the FAFSA for aid year 2026-2027, foreign income is required to be included in the Adjusted Gross Income (AGI) used to calculate Pell Grant eligibility.

Full Cost of Attendance Scholarships/Grants: Effective July 1, 2026, students who receive grants or scholarships from non-federal sources covering their entire Cost of Attendance are ineligible to receive a Pell Grant, even if otherwise eligible for the program.

High SAI and Pell Grant: Effective July 1, 2026, students will not be eligible to receive a Pell Grant if their SAI exceeds twice the maximum Pell Grant award which is currently $7,395.

Additional Resources